When Insurance Fails, Who Will Pay for Climate Damages?

Climate disasters are straining the insurance system. I4PC’s “Who Pays” report explains the rising costs facing insurers, governments, and homeowners.

Climate disasters are straining the insurance system. I4PC’s “Who Pays” report explains the rising costs facing insurers, governments, and homeowners.

Last week I spoke at the BC Climate Resilience Summit and hosted a fireside chat with Matt Price, Executive Director of Investors for Paris Compliance (I4PC). Our chat was centred around their recent report, Who Pays? Climate Damages & Canada's Looming Home Insurance Crisis. It's a short, incisive document that lays out the existential cliff that Canadian insurance is headed towards, and different responses that may emerge to the crisis.

I wanted to take some more time to dwell on that conversation and what the report highlights:

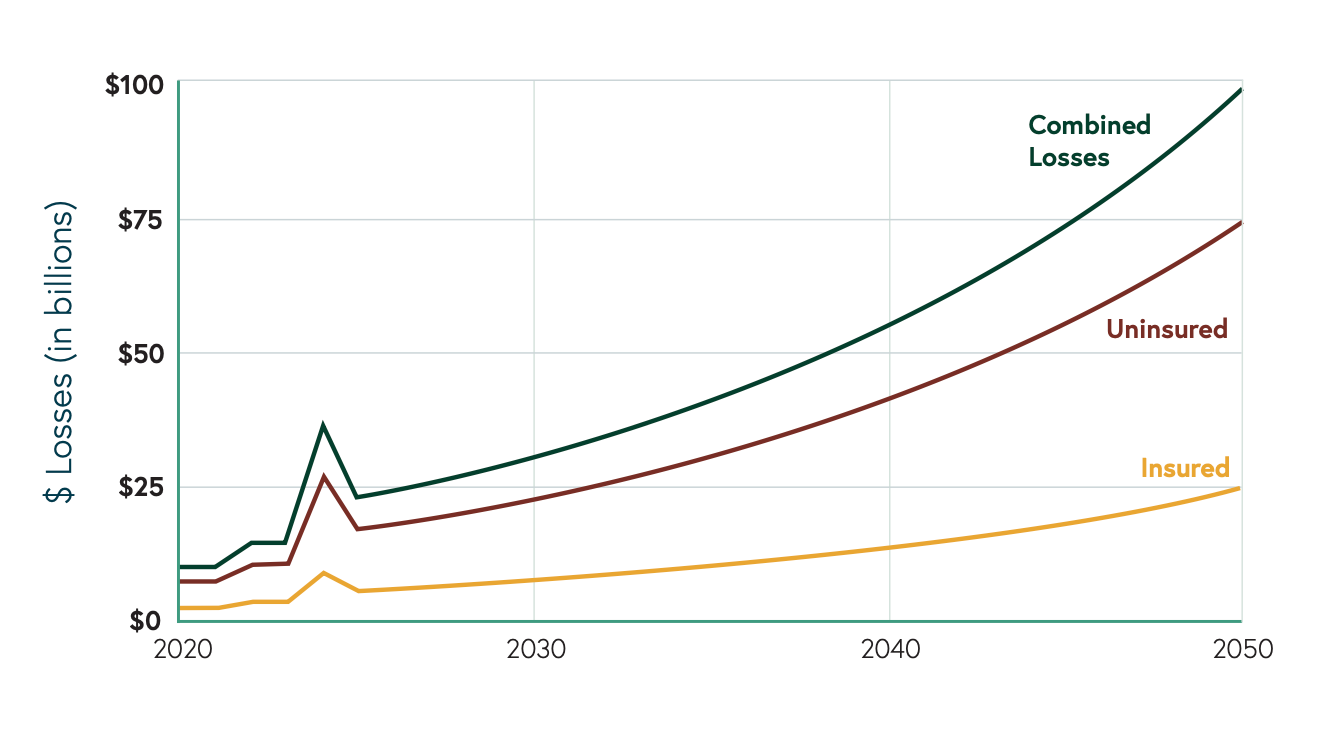

For those who follow the world of climate damages, the high-level numbers aren't new, but starkly and clearly stated: if you extrapolate out the current growth rate in climate-related damages, Canada could be looking at $100 billion a year by 2050 – frighteningly, with $75 billion of that coming from uninsured assets.

As much as we love to hate on (sometimes rightly) the insurance sector for high premiums, property and casualty ("P&C") insurance has had a dismal – and unsustainable – performance over the past few years. Quoting from the Insurance Bureau of Canada: "Personal property insurance market’s combined loss ratio was 101% for both 2024 and 2023, meaning insurers paid out $1.01 in claims and operating costs for every $1 they earned in premiums." [emphasis added] And this occurred even as premiums skyrocketed.

I4PC provides a sober, yet still haunting, summary of the problem we face:

As climate damages mount, insurance claims increase and these costs are being passed along to Canadian homeowners in the form of increased premiums and less coverage. This is a cycle with no clear end.

Most of the reading and discussions I have done around insurance and climate change, both at last year's Resilience Summit and elsewhere, have been focused on how we increase our spending on adaptation – the actions we take to reduce the risk or impact of climate damages. My dear friend Ana Gonzales Guerro at MaRS is often my thinking partner on this. It's a story for another time, but we're often dreaming about how you could start a community-owned enterprise that could build infrastructure at a profit and reinvest back into the same community (PUSH Buffalo being my favourite example).

But I4PC take a different tack. They describe both the rising rates and the money we spend on adaptation as a form of "cost transmission," not just for the insurance companies, but for fossil fuel producers.

As they say:

"Canadian households are currently stuck on a cost transmission cycle: each year extreme weather drives up insurance claims and the industry passes along these costs in the form of higher premiums, changes in coverage and deductibles for everyone."

In addition to the exorbitant rises in claims – where some high-risk areas have seen 60-70% rate-increases over a single year – there's also a growing phenomenon of a kind of insurance "shrink-flation," where the actual coverage is getting smaller and smaller.

While Canada is on the front lines of this, we're hardly alone.

Globally, the insurance market is getting battered. The flow of globally increasing risks meant that "[d]uring the 2023 renewal cycle, catastrophe reinsurance premiums for property in Canada rose by an estimated 25–30% for loss-free portfolios and up to 50–70% for portfolios that had experienced recent loss events such as a wildfire or flooding," according to I4PC.

This cost transmission isn't only about premiums, however. I4PC also argues that adaptation funding – building higher dykes, hardening homes to wildfires, and so on – is a form of cost-transmission, too. After all, these investments protect insurance companies' bottom line – and, as the graph above shows, they don't even insure all the things that actually get damaged.

There are glimmers of hope about different approaches: the Co-operators Insurance Group (disclosure: I have renters insurance with them) has both done some very forward-thinking work to support local hazard planning and risk mitigation through their Resilience Acceleration Lab. And Wawanesa Insurance, another cooperative-style insurance company, was also a co-sponsor of the Summit and teased future similar investments in the future. These are not systemic investments, but they could point to a future of co-investing with communities to reduce collective risks.

Other companies have been involved in more "informational" activities, that focuses more on sounding the alarm around climate change. For the first time at this year's Summit, I heard people actually express frustration over campaigns like this. Generic 'know your risks' communication materials – look out for forest fires! in Vancouver! or wherever! – started to look like "elaborate forms of victim blaming," as one person said to me, if the information didn't help you take action.

At a more systemic level, the insurance industry's push for national policies, like federal flood insurance (now in its ninth year of being promised), could also function as a way for companies to offload their riskiest, least profitable policies.

Done poorly, a program could look like the California-style FAIR Plans that exist across the US and struggle to stay afloat because they only have the lowest-resource, most endangered properties in their risk pools.

Things also become more complex when the question of "clean hands" is raised.

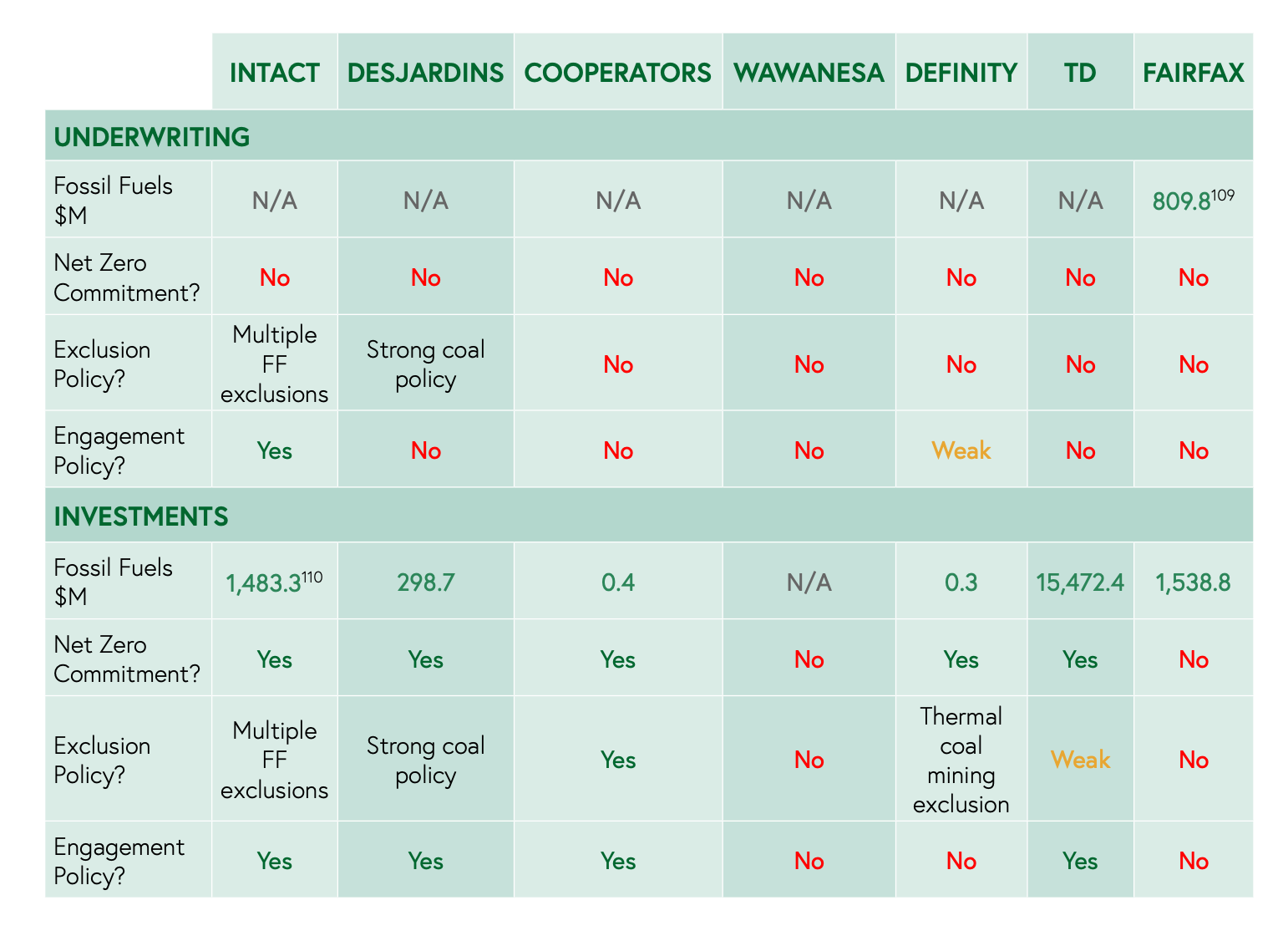

As I4PC has previously argued, although most insurance companies talk about climate change a fair bit, many are also still investors and insurers of the fossil fuels industry.

While international insurance companies (and especially the reinsurance companies) are getting more aggressive on net zero, I4PC's Playing with Fire report found large gaps between talk and action, with some of the largest companies, such as Fairfax, not even having a net zero target and almost everyone continuing to underwrite fossil fuel infrastructure.

As is always the case in Canada around the energy transition, the story is complex. The Co-operators are owned in part by the Federation of Alberta Gas Co-ops, for example. And while they and others can avoid big investments in fossil fuels, underwriting some aspect of fossil fuel infrastructure (e.g., drilling, pipeline services, etc.) becomes a trickier undertaking. Everyone's implicated in the transition, and, with varying levels of effort and speed, everyone's trying to figure out how they get to the other side whole. But some, as the table above shows, have more pep in their step than others, to put it politely.

So if we accept the premises that (1) insurance continues to get riskier and therefore costlier, (2) companies have limited tools and willingness to spend to reduce those risks, and (3) those costs will increasingly be born by taxpayers, what's society to do?

Enter attribution science.

As I4PC says of it:

Attribution science was developed to answer the question: did climate change cause or impact this event? For example, climate change made Québec’s 2023 fire season around 50% more intense, and seasons of this severity at least seven times more likely. It has now evolved into end-to-end attribution frameworks that connect emissions from identifiable sources directly to measurable physical and economic damages, which can be applied to meet legal standards for admissibility.

The science, they argue, has matured spectacularly in the past few years. As the evidence of how much burning fossil fuels has contributed to major disasters grows, one can begin to assign responsibility to fossil fuel producers to help recover damages.

I4PC takes both a moral and a pragmatic framing: greenhouse gas emissions drove climate change; fossil fuel producers largely generated those emissions; they still have a great deal of money; therefore, they should pay significantly for damages. Beyond helping people who have lost (or could lose) their homes, I think there's also a more cynical motivation at play, too:

Governments, banks, and residents are very unlikely to accept the outcome of an "uninsurable world." We have seen that in Florida and California already. Without insurance, you don't get mortgages, and without mortgages, you don't get homes – and building and owning homes is, sadly, one of the central pillars of North American wealth. Everyone is motivated to keep the flow of money moving into real estate (B.C.'s largest industry, as I reminded the room), and so by hook or by crook, as costs bear down on that industry, everyone will be looking for a way to make themselves whole.

With record profits, large fossil fuel producers will no doubt come into the public's crosshairs.

It's already happening, according to I4PC:

More than 100 climate-related lawsuits have been filed annually from 2017 to 2023, ranging from cases alleging inadequate climate risks disclosure to investors to cost recovery claims. Advances in attribution science are being used by several U.S. governments to seek compensation from oil and gas companies for physical damages linked to historical emissions and the industry’s role in delaying action on climate change.

These could take several forms:

At the time of the writing, at least least 25 cities, counties, and states in the US and many others globally are involved in lawsuits of this type, not to mention the other consumer-led actions around damages occurring globally. Canada has precedent for this, I4PC argues, through the tobacco cases in the 2010s, which have brought in billions into the public health systems in the provinces.

I wasn't trying to be glib when I titled my session with Matt "when do we press the big red button on climate damages?" I meant it as a sincere question, though perhaps an incomplete one.

In 2025, New York signed a piece of "superfund" legislation to force large fossil fuel companies to give them payouts to support adaptation infrastructure; it was the second state to do so after Vermont in 2024. Even though the law is being challenged in court, it will not be the last.

I won't go into detail laying out the superfund structure, but Purdue has a wonderful overview of New York's approach that's worth exploring.

In the United States, these laws are being challenged directly by Republican-governed, oil and gas-producing states. Everyone understands the cataclysmic risks to the industry should one or both of these programs survive in some form. In Canada, especially in Alberta, these risks are existential.

I pondered what would happen in Canada if, for example, a Quebec or B.C.-based class action lawsuit emerged and was then folded into legislation. How profound of a national unity crisis might that create? Or would a federal superfund be able to manage those risks and payouts? Importantly, how would these kinds of payouts also intersect with the hundreds of billions in unfunded oil and gas cleanup costs?

At the same time, there are also lessons in the tobacco payouts, with some people critical of how the now-hundreds of billions of dollars paid out by cigarette companies were put to use. This is where superfund legislation, not just large class-action lawsuits, could structure the use of funds more appropriately.

Insurance companies, certainly, could also play a role in this, leveraging their data on policyholder risks to support effective adaptation planning by the government. We've already seen limited versions of this, but visibility into where climate damages will hit hardest also creates other risks in the property market – this is why Canadians still haven't seen parcel-specific flood mapping, for example.

The most important thing to say about everything here is that these laws are not (only) about moral responsibility for climate change; they are about costs. Because climate change is expensive.

As the costs of both immediate climate damages and the measures we take to prevent them grow, pressure will build in the system. The B.C. Government estimates that climate damages in 2025 cost over $300 million, as one example. Residents, insurance companies, and governments will all have incentives to find someone else to share the load. The pressure to go beyond taxpayers will continue to build.

As I implied in the title for my conversation with Matt, the most important question is not whether or not someone will use the above tools to protect the insurance system; it's who, and most importantly, how someone gets there first.

Strategist, writer, and researcher.

No spam. Unsubscribe anytime.